The Week Ahead

April 9, 2023

One of my good friends texted our group at the end of last week, “Gosh guys I love our country but man this week was a real dystopian freak show.” (Pretty sure there was some sarcasm in there.)

If you’re feeling the same way, take a minute to consider what we accomplished.

First: Last week in Wisconsin, voters, especially young voters, turned out and elected a Democratic Supreme Court Justice in a pivotal state, likely assuring better outcomes on important issues like voting rights and abortion.

Second: National outrage brought attention to Tennessee, giving a national platform to the voices of expelled legislators. The two, Justin Jones, representing Nashville, and Justin Pearson, representing parts of Memphis, can be reappointed to their positions by local authorities and cannot be expelled again for the same “offense.” They should be back in office soon. Something tells me their constituents are going to want them back.

The blatant racism behind their expulsion while the legislature (narrowly) failed to expel Gloria Johnson, a white legislator, was a wake-up call. The allyship between the three legislators was an inspiration. Sometimes good things can come from an outrage. Now that the country’s attention is focused, it’s less likely that other efforts to unfairly, and illegally as in Tennessee, silence progressive voices will go largely unnoticed. We are, as they say, woke. It will be easier to focus public attention on the interconnection between efforts across the country, whether it’s Tennessee, or Jim Jordan’s efforts to kneecap Alvin Bragg’s prosecution with subpoenas and a congressional investigation, or Georgia’s new law that gives conservatives the ability to fire progressive prosecutors like Fani Willis. Florida Governor Ron DeSantis used a pretext to fire Tampa prosecutor Andrew Warren last summer because he didn’t like his stance on abortion. Although the public interest in that abuse of power died down quickly, in today’s climate, reporting that DeSantis has set his sights on another prosecutor, a law professor who ran for office successfully as a criminal justice reform advocate, is likely to garner more scrutiny. So, good trouble.

Third: The Washington state senate passed a measure that bans the production, sale, and importation of assault weapons. The bill is on its way to the governor’s desk for signature. Voters and activists did that together. Voters used their collective power to elect representatives who reflected their views, and activists turned up the heat and kept it on until the measure passed.

If we remain informed on the issues, active on important measures we expect our elected officials to take on our behalf, and focused on voting despite the amped-up efforts by conservatives to suppress votes by those who disagree with them, we can succeed. It takes patience and persistence, and that’s not always easy. But it’s necessary to do the work ahead of us to ensure our rights are protected. The MAGA caucus and its leader are one of the most anti-democratic developments in our recent history, and democracy is still fragile. Our job as citizens is to out-think and outlast them, using the rule of law to re-establish our norms.

With that in mind, there are two key issues on the radar screen for next week.

I. What happens this week with the dueling orders from two federal judges on mifepristone?

Shortly after Judge Kacsmaryk, in Texas, entered a nationwide injunction against the abortion drug mifepristone, another federal district court judge in Washington state entered a contrary order in a case brought by 17 attorneys general in blue states. He ordered the FDA to keep the drug available in those states.

It’s complicated—the FDA sets national standards, so the idea that it lets approval stand in 17 states while revoking it in the others is inconsistent with how the agency usually functions. DOJ hasn’t yet said how it will handle the split decisions—Washington state is in the 9th Circuit Court of Appeals and Texas in the 5th—and what position it will take on the order in the Washington case.

Many of you have asked about nationwide injunctions and how a judge sitting in one district can enter an order that binds the entire country. An injunction is a form of equitable relief, which means something other than money damages in a civil suit. There are well-established standards for granting them, which you may be familiar with from many of the cases we’ve discussed in the past year, among them Donald Trump’s request that a district judge in Florida enjoin DOJ from reviewing items seized in the search of Mar-a-Lago. Injunctions aren’t a final decision in a case; rather, they typically involve a request by a party to prevent something they think is legally wrong from happening while litigation is proceeding.

Injunctions are reserved for extreme situations where the party seeking one can prove they (1) have a substantial likelihood of winning; (2) will be irreparably injured without the injunction; (3) will suffer an injury that outweighs any harm to the other party; and (4) the public interest merits an injunction. The term “nationwide injunction” isn’t defined in court rules or federal statutes, or by the Supreme Court, but it’s used with some consistency by the courts to refer to an injunction against the federal government that prevents it from implementing a challenged law, regulation, or other policy, even as to those who aren’t parties to the lawsuit—in other words, it applies to everyone, and nationwide, not just to the parties and in that jurisdiction.

Judge Thomas Rice in Washington state declined to enter a nationwide injunction when he ruled on the attorneys general’s case. He entered a more limited injunction that applied only to the states they represent, writing that when a court determines that an injunction is warranted, the relief it grants should be no more burdensome to the defendant than necessary to provide relief to the plaintiffs. He reminded the 17 state attorneys general who brought the lawsuit that the purpose of an injunction isn’t to decide the merits of the case before the court, but to balance the parties’ rights while the litigation is pending.

Judge Rice’s ruling was much more modest than Judge Kacsmaryk’s, requiring the FDA to keep mifepristone on the market only in the states that sued, noting that suspending the FDA’s approval of mifepristone would alter the “status quo.” Despite considering essentially the same situation as Judge Kacsmaryk’s ruling, he declined to enter a nationwide injunction. Judge Rice noted, as we discussed Friday evening, that post-Dobbs, abortion restrictions “vary state-by-state,” so an absence of nationwide uniformity is not surprising, and the rare remedy of a nationwide injunction not warranted. In an apparent slap at the Texas decision that just barely preceded his, he wrote that a nationwide injunction is “inappropriate where there is the potential for competing litigation,” a view that should be persuasive on appeal given the rules, but as we’ve also previously noted, this Supreme Court seems to use different jurisprudence in service of restricting abortion rights.

In the Texas case, the FDA argued that injunctions are typically used to preserve the status quo during litigation. But Judge Kacsmaryk’s order, in the words of the agency, “would upend the status quo” that has held for more than 20 years. No matter that other drugs were approved the same year as mifepristone with fewer years of data and that usage of the drug over the past 20 years bears out its safety. The irony of the Judge’s ruling is that it ends the legal availability of a drug on the basis of unproven and untrue allegations of inadequate safety protocols, in the meantime making women’s health more precarious, especially in cases of medically necessary abortions or incomplete miscarriages.

This week we’ll be watching for DOJ’s position in the Washington litigation and to see just how quickly the cases land before the Supreme Court. There is a legal mechanism in 28 U.S. Code § 1254 that allows cases to leapfrog from an appellate court to the Supreme Court once a notice of appeal is filed but before a decision is made. Once that legal maneuvering is complete, it will be up to SCOTUS to determine the scope of any injunction while the litigation proceeds on the merits. If the Texas order stands, pregnant people in America, and women in general, will have less certainty than at any other time since Roe v. Wade about their ability to make key medical decisions about their health and their future.

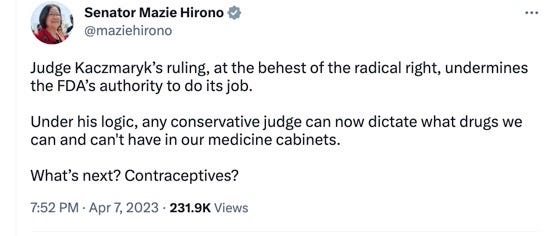

We don’t know where this ends, but Hawaii Senator Mazie Hirono offered this speculation:

II. How should we think about the Trump indictment as the case enters discovery, where prosecutors turn over information about their case to the former president’s lawyers, in a process that will be largely opaque to the public?

First, we’re going to need to get used to being patient. Though it’s likely there will be litigation over some preliminary issues before the court-scheduled hearing in December, there won’t be a trial anytime soon and certainly not this year. For those of you interested in Trump-related trials, however, E. Jean Carroll’s defamation lawsuit against the former president begins later this month in federal court in New York.

Since we have some time, we can begin to understand the District Attorney’s theory of the case and some of the legal challenges the case faces. It’s completely normal, by the way, for legal issues to be raised before the trial court in advance of a prosecution. Don’t expect all of these issues to be frivolous, like the lawsuit Trump filed in Florida after the search of Mar-a-Lago. There will be some legitimate issues to iron out, although the more I read, the more it confirms my initial sense that the Manhattan DA has the better of these issues.

You’ll recall the horde of commentators who rained down hellfire and brimstone and were sharply critical of the indictment before they’d had a chance to read it. Now they, but also some pundits who don’t consider themselves to be Trump supporters, are predicting there are legal arguments that will be fatal to the prosecution without careful study of the issues. Most of the concerns suggest that there are difficult, thorny issues that, in some cases, have not been previously decided by the courts. But prosecutors in Manhattan have been hard at work for months, really for years, working the problems before concluding they had a case that was solid enough to proceed. So don’t be too alarmed by the naysayers.

In addition to a whole slew of challenges about whether the facts are sufficient to prove the crimes Trump is charged with, we’ll hear a lot about legal doctrines like preemption (which will come into play on the issue of whether Bragg can use a federal crime as the crime Trump intended to commit when he made the false entries in his business records), as well as the issue of whether the congressional committee that has begun issuing subpoenas in the matter is entitled to interfere in an ongoing state prosecution. The answer to that is clearly no, but don’t expect the law to prevent Jim Jordan from making life as difficult as possible for Manhattan DA Bragg.

Expect to continue to hear many commentators complaining that prosecutors didn’t fully explain their theory of the case in the indictment, specifically, what the charge that converts the misdemeanor business records fraud into a felony is. Of course we’d like to know about the prosecution’s theory of the case, but informing the public isn’t their job when they write an indictment. Their job is to track the elements of the statute, use the correct if complex legal language, and produce a document that will withstand scrutiny both at trial and on appeal. That doesn’t always make it easy for people in the public to understand, especially for people without a legal background, but the most important thing is for them to do it right, which means in ways that will stand up on appeal if there are convictions.

So we wait. Under New York law, prosecutors will disclose all of the information the law requires them to in the course of providing discovery to Trump’s lawyers. But they are entitled to wait on some points, most importantly the issue of what the additional crime is. They’ll make that election from among the available choices at a time that both protects the defendant’s right to have notice of the charges against him and maximizes the strategic interests of their case. Interestingly, no one, not even Trump himself, seems to be saying that he didn’t do it. Instead, the argument is that the prosecution is politically motivated, that the charges aren’t significant, and that perhaps they were brought too long after they occurred—that the statute of limitations for bringing them has run.

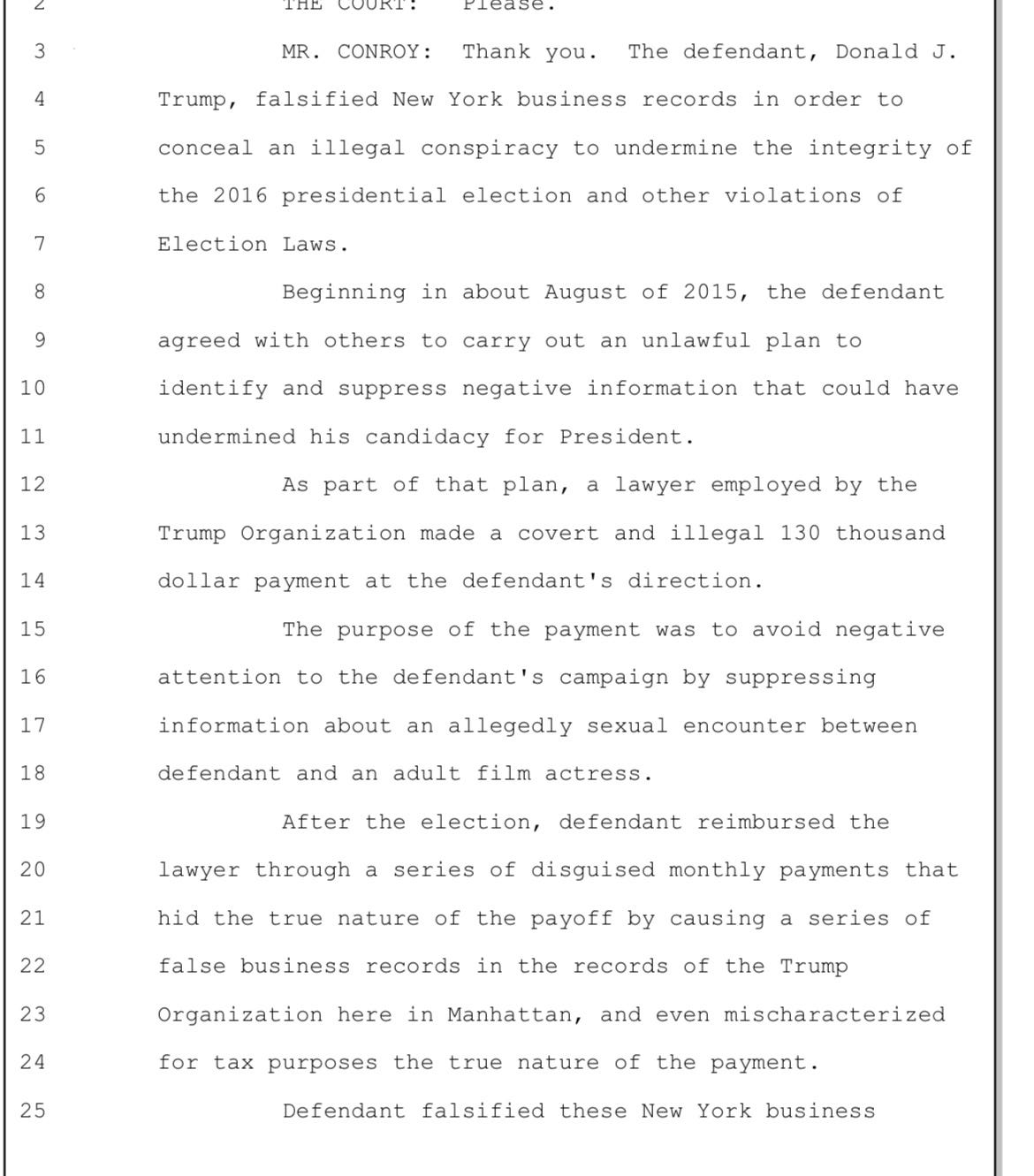

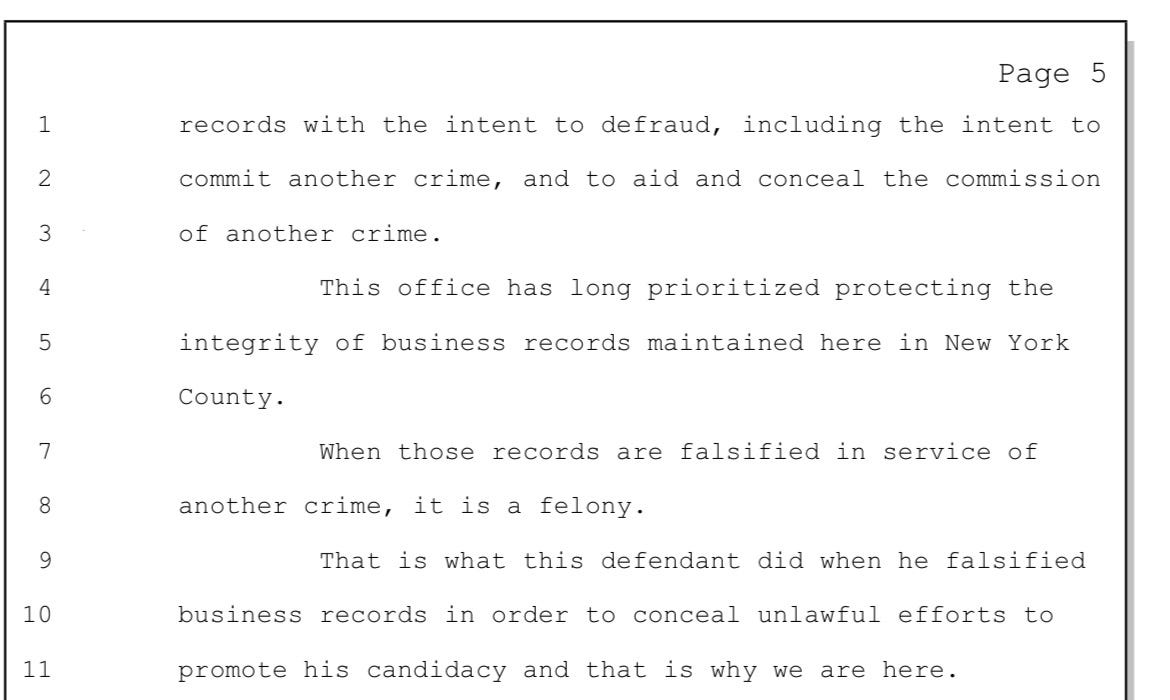

Chris Conroy, an Assistant DA who spoke to the court at arraignment, summed up the case this way: “Trump falsified New York business records in order to conceal an illegal conspiracy to undermine the integrity of the 2016 presidential election and other violations of Election Laws.” A jury heard the evidence and decided there was sufficient evidence to indict. There is no way that an experienced prosecutor like Bragg would have brought the case if it was a close call, considering himself lucky to get an indictment. Prosecutors don’t focus on the probable cause standard that grand juries use, but on whether they have proof of guilt beyond a reasonable doubt to win at trial. In a case like this—it’s been said a thousand times, but it’s still true—if you come at the king, you’d best not miss. Bragg’s team has almost certainly walked through and resolved all of the issues the pundits and the public are only just now contemplating.

Give it some time. (I can hear y’all shrieking at me for saying that, but it’s how prosecutions work.)

We’re in this together,

Joyce

I am a dedicated fan and tax lawyer/CPA (since 1976). Many of your colleagues are discussing the possible Trump tax fraud case (the “in furtherance” crime) incorrectly. I understand it’s complicated but try this:

Here is some further clarification on the potential New York State tax fraud case that Alvin Bragg, New York County District Attorney, could bring against Trump, or a constituent entity within the “Trump Organization.” I use the term “clarification” loosely, because tax evasion—tax fraud—depends on a byzantine set of facts and legal structures intended to deter detection and make it difficult to present the case to an average juror.

Remember that the false books and records charges under New York law are mere misdemeanors unless the falsifications were undertaken in furtherance of, or to conceal, another crime. The person falsifying the business records need not have committed that other crime. Said another way, if Trump falsified his business records, or directed the falsification of the TO’s business records, to conceal an act of tax evasion by another person, his misdemeanor becomes a felony.

Did anyone else commit tax evasion? We know from the Statement of Facts that Michael Cohen did not. Indictment No. 71543-23 alleges that Donald J. Trump made a series of monthly payments to Michael Cohen for the economic purpose of reimbursing him for the hush money payment he made to Stormy Daniels at Trump’s direction and on his behalf. The reimbursements went from the $130,000 paid to Ms. Daniels to about $430,000 because of the need to gross up Cohen for taxes and interest. Cohen needed the gross-up because he knew he was going to report the payments as income and that he couldn't deduct them.

As the indictment alleges, Cohen issued invoices each month to the Trump Organization (the “TO”) for legal services pursuant to a fictitious retainer agreement. Notwithstanding that Cohen passed the invoices to the TO, according to the indictment, Trump paid the monthly installments out of his personal checkbook and out of a checkbook maintained by the “Donald J. Trump Revocable Trust.” The revocable trust is a “pass-through entity,” which means that it is ignored for tax purposes; its income and deductions are passed through directly to Trump’s individual tax return.

To attempt to clarify, Cohen issued the invoices to the TO, but Trump paid them—not the TO.

So, stopping there for the moment, the scenario where Trump writes a personal check to Cohen is just a false records charge. It was not a payment for legal services. It was just falsely labeled as such. Unless Trump took a deduction for the payment somewhere on his return, he committed no tax evasion by writing the check to Cohen.

But we can’t stop there, because the indictment alleges more facts that are difficult to reconcile with the fact that Trump wrote the checks from a personal or revocable trust checking account. The Trump Organization got involved in the process. Cohen issued the invoice to the Trump Organization (“TO”). Jeff McConney, the then-controller for the TO, “forwarded each invoice to the TO Accounts Payable Supervisor. Consistent with the TO Controller’s initial instructions, the TO Accounts Payable Supervisor printed out each invoice and marked it with an accounts payable stamp and the general ledger code [GL account number] 51505 for legal expenses. The Trump Organization maintained the invoices as records of expenses paid.” Statement of Facts, Par. 30.

Statement of Facts, Par. 31 further states that the TO Accounts Payable Supervisor recorded each payment in the TO’s general ledger, presumably in account 51505, as a payment for legal expenses. The TO prepared and preserved “check vouchers” for each payment. Check vouchers are a normal business record kept when a business writes a check to a vendor. The vouchers consist of the underlying invoice, the account to which it was assigned, and the record of approvals for the cash outlay, which all raises a very interesting question:

Why would the corporate accounting systems get involved if Trump were making the payments out of a personal or revocable trust checking account, as opposed to one of the corporate entities making the payment? If Trump wrote the checks out of his own account, he would not need any vouchers.

The answer could be that Trump could not take a deduction for a payment disguised as personal legal expenses, but a corporate member of the TO surely could try. Thus, the invoices went to the TO, but the payment came from Trump. The fact that Trump made the payment from a personal checking account is irrelevant. A deft series of bookkeeping entries (i.e., journal entries) could account for the Trump personal check as a cash injection into the TO followed by the TO’s outlay of the expense.

On paper, it looks like Trump, as a matter of convenience or whatever, laid out cash to cover an expense of the TO. The economic reality, however, was that Trump paid the Cohen invoices, but the TO booked them to get an illegal deduction.

The TO (or a member company) committed tax fraud. Trump’s false business records misdemeanor was committed to conceal that tax fraud, thereby creating a felony.

If, because of the tax character of the TO members, that deduction got indirectly passed back to Trump, he committed tax fraud.

The allegations in the indictment and statement of facts implies that Bragg already has the vouchers, the general ledger account number, and copies of Trump’s checks. My guess is that Cohen gave the grand jury the copies of the Trump checks. Cohen kept records of everything. I am also guessing that McConney, who was a key evidence source in the previous payroll tax trial of the TO and Weisselberg, gave this grand jury the accounting trail and the "account-grouping" worksheet that got the numbers in the general ledger (including account no. 51505) into the corporate and partnership returns. Weisselberg is in prison, and McConney, who no longer works for the TO, most likely does not want to go to prison.

Excellent perspective. I do have one clarification. The Washington state assault weapons ban needs to go back to the House before going to the Governor since the Senate made a couple modifications. It passed in the House once. Let’s hope it does again.